Market Morsel

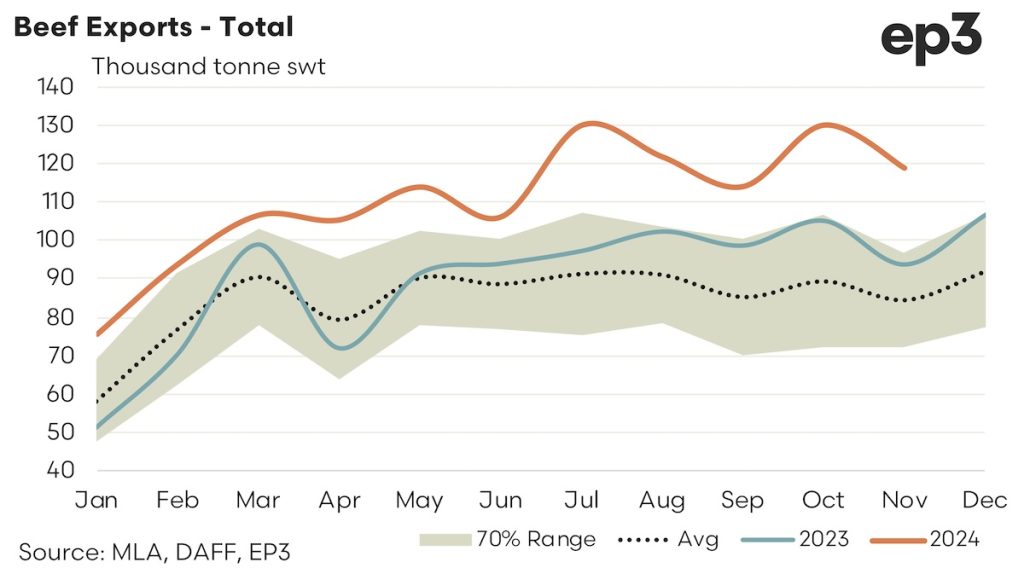

Monthly export figures released by the Department of Agriculture shows November 2024 shipments at 118,878 tonnes, a 9% drop from October’s record-breaking 130,048 tonnes. However, November exports were still 27% higher than the levels seen in November 2023 and nearly 41% above the five-year average for November.

Year-to-date exports have now reached 1.216 million tonnes, up a significant 25% or 241,000 tonnes higher when compared to the same time period in 2023. With only December remaining, the 2024 export volume is poised to surpass previous records of 1.22 million and 1.23 million tonnes, set in 2015 and 2016 during the drought-driven cattle turnoff.

A summary of the top trade locations, in order of top market share for 2024, is as follows:

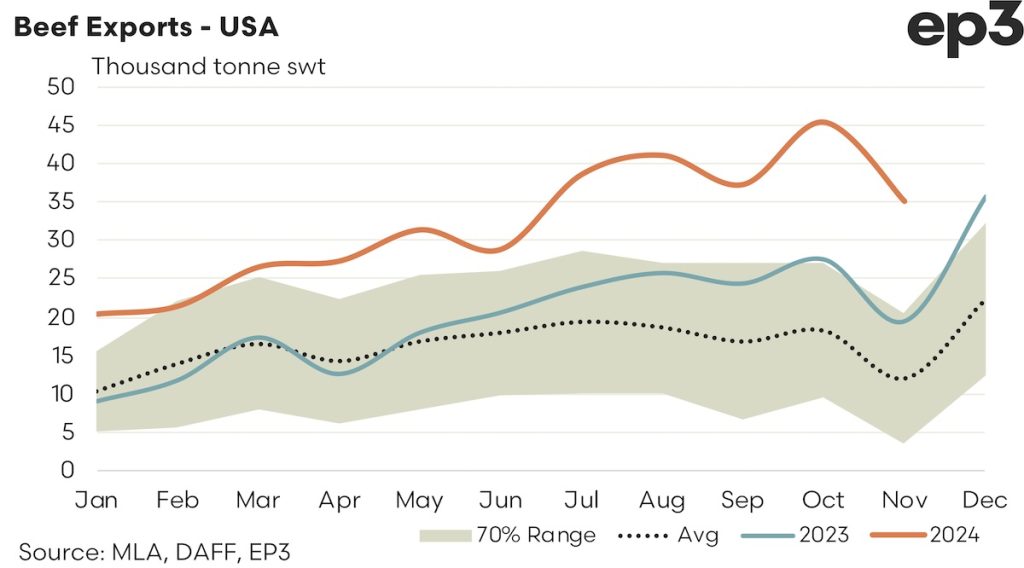

USA – There was a 23% drop in beef export flows to the USA from Australia during November to see 35,026 tonnes shipped over the month. As the seasonal average trend identifies it is not uncommon to see a drop in US demand for beef from Australia in November some years and it is not something to be too concerned by as an Aussie beef producer or exporter as the demand from the USA will remain firm into 2025 given their supply picture. The USA has imported 352,440 tonnes of Australian beef so far this year, up an extraordinary 68% or 142,000 tonnes on 2023. Declining US herd numbers, reduced beef production/cold stores and high cattle/beef prices are driving demand for offshore alternatives.

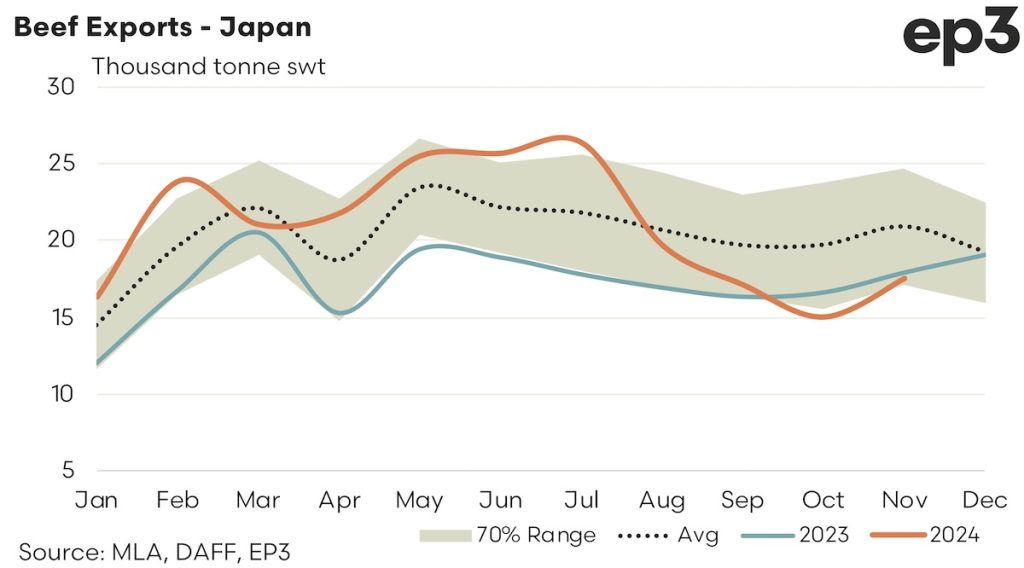

Japan – November shipments to Japan were 17,515 tonnes, a 17% gain from the levels seen exported during October 2024 but only 2% lower than the previous November. Year-to-date exports to Japan reached 229,522 tonnes, up 22% and compared to the five-year average levels for November the current trade flows are sitting at levels that are 16% softer.

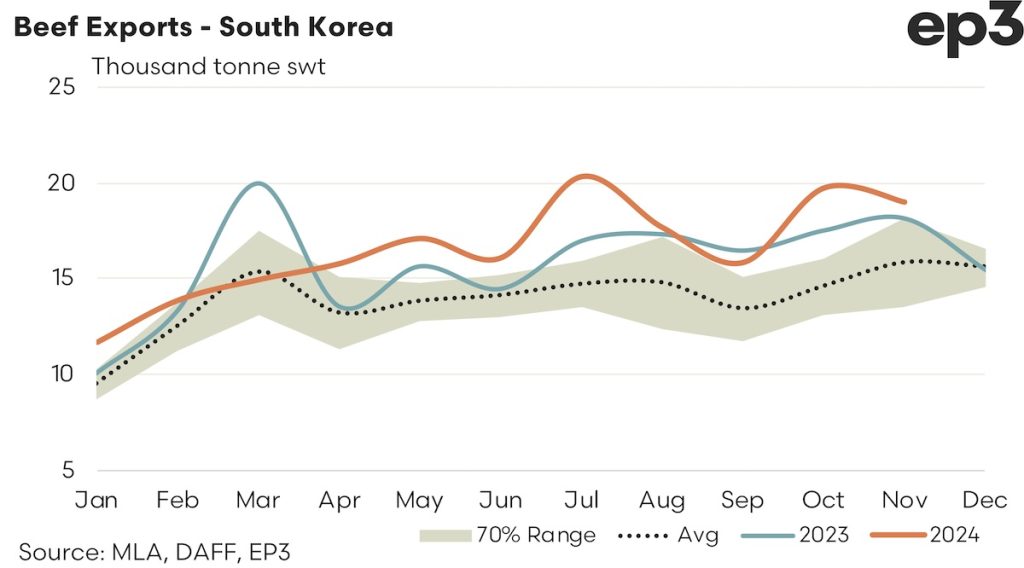

South Korea – November exports reached 19,001 tonnes, slightly below October’s volumes but still 5% higher than November 2023. Compared to the five-year average for November the beef trade to South Korea currently sits 20% higher and on a year-to-date basis, South Korea has taken 182,000 tonnes, which is a 5% increase on last year.

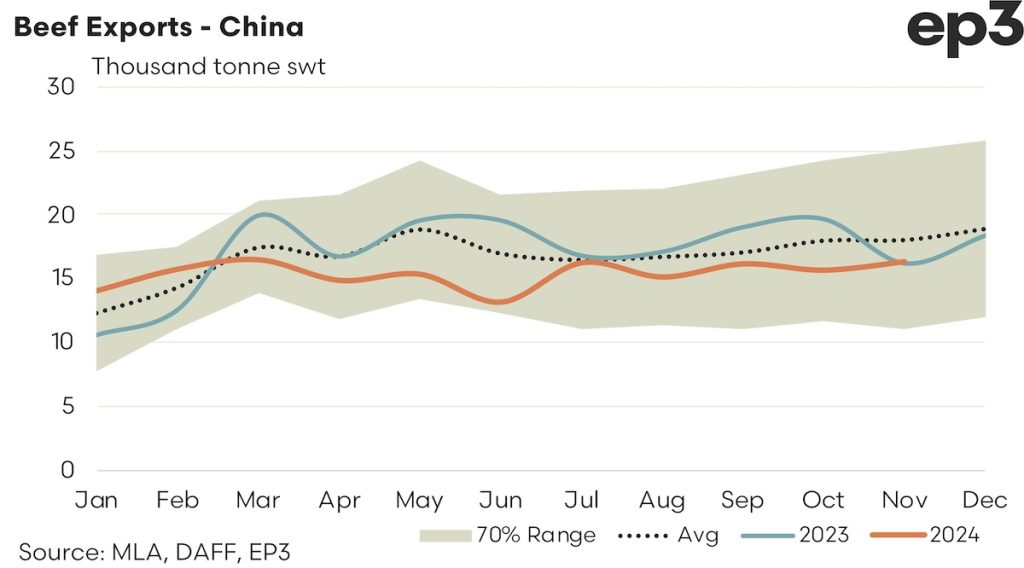

China – Ongoing economic challenges have impacted trade, with November exports to China totalling 16,337 tonnes. Year-to-date figures reached 169,368 tonnes, down 10%. The November trade levels remain below the average seasonal pattern but have come in pretty close to trade levels seen during November last year.

Victoria, the largest processor of lambs in Australia, also showed notable movements, albeit with a steadier trend in sheep processing. The sheep slaughter index remained high but dropped slightly from 95% in October to 92% in November. This minor decline may reflect some shift in processor focus as lamb supplies ramp up.

The Victorian lamb slaughter index rose from 52% in October to 73% in November, reflecting growing availability of lambs as the season progresses. Victoria’s consistent processing capability ensures it remains a cornerstone of Australia’s lamb industry, and the uptick in lamb slaughter is a positive sign for producers after a relatively slow start to the season.

Tasmania stands out as the only state where lamb slaughter surpasses sheep processing in relative terms. The sheep slaughter index rose significantly from 32% in October to 76% in November, reflecting a strong recovery in processing volumes. However, the lamb slaughter index reached an impressive 75% in November, up from 46% in October.

Western Australia maintains its dominance in sheep processing, with the sheep slaughter index reaching 95% in November, up from 32% in October. This substantial increase underscores WA’s strategic role in meeting global mutton demand, particularly given its proximity to key export markets in Asia.

Lamb slaughter in WA, while not as prominent as sheep, also showed an increase, with the index moving from 46% in October to 56% in November. This aligns with broader national trends as spring lamb supplies come to market.

In South Australia, the sheep slaughter index dipped slightly from 90% in October to 88% in November, but lamb processing saw a consistent rise from 42% to 50%. These trends reflect SA’s balanced approach to meeting demand for both sheep and lamb.

Queensland, though a smaller player in sheep meat processing, showed stable activity. The sheep slaughter index moved from 75% in October to 86% in November, while the lamb slaughter index saw a modest decline from 74% to 62%.

The substantial lift in lamb slaughter across most states reflects the arrival of spring lamb supplies, a critical factor in Australia’s livestock calendar. This seasonal boost has allowed processors to increase lamb volumes, even as sheep slaughter remains historically high due to strong export demand for mutton.

Export markets, particularly China & Malaysia, continue to drive demand for sheep meat, with mutton favoured over lamb in many cases due to its price competitiveness and suitability for traditional dishes. This has kept sheep slaughter at elevated levels, especially in WA, which are well-positioned to capitalise on this trend.