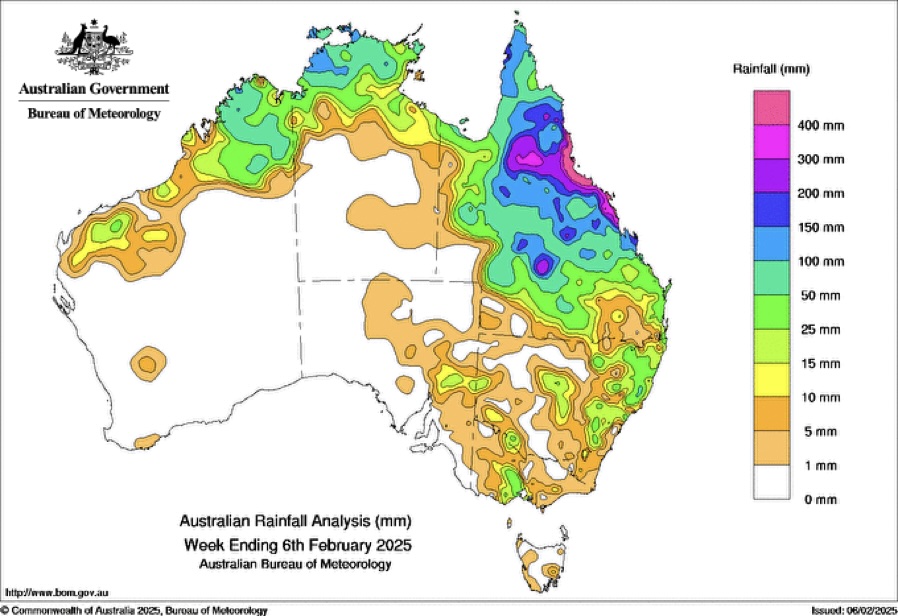

Widespread falls extending well into southern QLD has provided some support to hold the markets this week, expect that to continue as cattle supply shortens.

Key Points

- Focus this week is the widespread falls in QLD, which has tightened supply in the state this week and provided some stabilization and slight improvements in the market, particularly the restocker cattle.

- Southern markets continue to remain pressured by hot and dry weather, with further downside exposure on price through February due to this.

- Good demand in southern markets for grassfed finished cattle expected to be strong in 2025 due to reduced supplies.

Error in US Calculation

- Last week in this note I stated a draft of feeder steers sold in the US were worth A$7,880/head – this calculation was incorrect, I’d formatted cells wrongly on the calculator I use.

- Correct figure for the spot value cattle as of last week was actually A$3,677 per head.

Supply

- Beef exports for Jan-25 reached their highest January on record, at 81,050 mt, surpassing the previous high set in Jan-20 by 1,830 mt and were higher compared to Jan-24 by 7.2% or 5,466t.

- As outlined in the 2025 StoneX Australian Cattle Outlook report last Tuesday, I expect to see more of these type of results this year, the next big month should be March.

- The month January saleyard cattle numbers were 56% or 104,000 head higher than the 10-year January average and 44% or 89,300 head higher than Jan-24.

- The premise of rain following two big weeks for the major saleyard centres of Roma & Dalby saw tighter numbers in these yards this week, with solid falls which were much needed across large areas of QLD being beneficial over the week.

- Next week – with good falls in a large area of QLD this week, tighter supply is expected as a reaction, similar dynamics expected for northern NSW.

Demand

- These rains should aid demand in QLD for restocker cattle, with plenty of solid falls in areas which needed it, setting some up for a solid grass budget to trade cattle. We’re already starting to see evidence of this in QLD restocker markets this week.

- Feedlots are comfortable at present with numbers which is seeing some softer demand, dependent on supply forwards that may continue which is why I see stable to slightly softer prices in the coming weeks.

- Processor demand remains solid for the finished cattle, there should be some good demand for grassfed bullocks in 2025, particularly in the south due to lower supplies.

Price

- I can see southern markets coming under sustained pressure as Q1 2025 progresses, without genuine, widespread falls for southern regions impacted by drought, dry condition, higher supply and a lack of demand from producers will pressure pricing.

- Considering the QLD rains, unless this is sustained and follow up falls eventuate, this market firming up may be a blip on the radar, pressure to pricing may return forwards once the market shakes out the effects of these recent falls. Time will tell.

- Saleyard markets back anywhere from 10c to 48c/kg lwt from where the market opened 2025 a month ago.

- Feeder pricing remained flat generally this week with some slight downside, a few NQ’s or feeders staying out of the market, very much a state specific outcome this week with NSW softer again by 8c whereas QLD held firm.

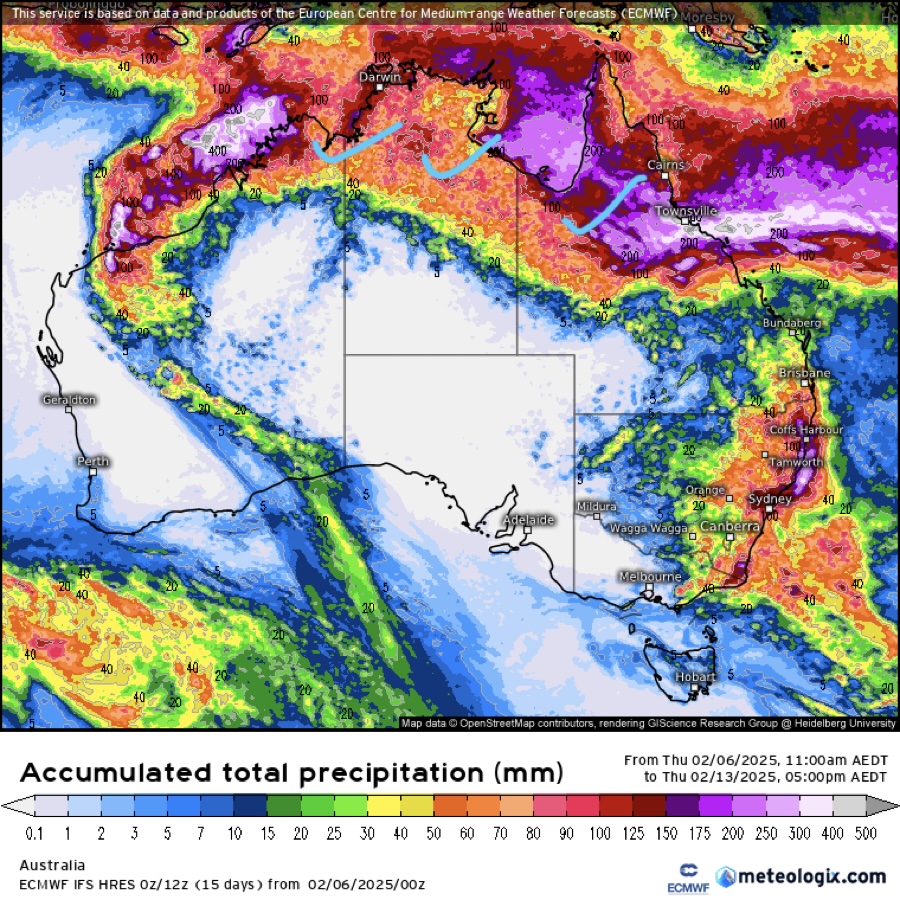

Weather

- A drier and hotter bias for the remainder of February is expected across most of the eastern seaboard, with rainfall focused for the northern regions as is seasonal.

- The wet season is expected to finally ramp up for the north, setting the regions up for its 3rd consecutive above average wet.

- 7 day accumulated precipitation map below for ECMWF Forecast – as above, focus becomes the north which is positive for these cattle regions.

Ripley Atkinson | Australian Livestock & Commodities Manager

M: +61 427 417 803

www.stonex.com | ripley.atkinson@stonex.com

StoneX Financial Pty Ltd (ACN 141 774 727 | ABN 50 141 774 727)

Suite 28.01 | 264 George Street | Sydney | NSW | Australia

NASDAQ: SNEX

StoneX Disclaimer

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI. StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorised to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorised & regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorised by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.